How to Improve Your Credit Utilization Rate

October 20, 2023Credit utilization is an important aspect of your financial health, reflecting the extent to which you're currently utilizing the credit available to you.

Whether you're seeking a prime-rate mortgage or a business loan with favorable terms, maintaining a low credit utilization ratio is essential. In this blog, we delve into the mechanics of this ratio and its implications for your access to credit.

What is a Credit Utilization Ratio?

Your credit utilization ratio, often expressed as a percentage, is a measure of the revolving credit you currently utilize compared to the total revolving credit at your disposal.

Revolving credit accounts, such as credit cards and home equity lines of credit, offer a continuous source of credit for various transactions, which can be repaid and reused.

Revolving credit refers to an account that enables you to borrow money repeatedly, up to a predetermined limit, and repay it over an extended period; while installment credit involves fixed, regular payments toward a specific loan amount

It's advisable to keep your credit utilization under 30% to prevent any adverse effects and promote positive credit score development. Lenders typically prefer to see borrowers using no more than 30% of their total available revolving credit. Exceeding this threshold may raise concerns about your repayment capacity.

How to calculate your credit utilization ratio

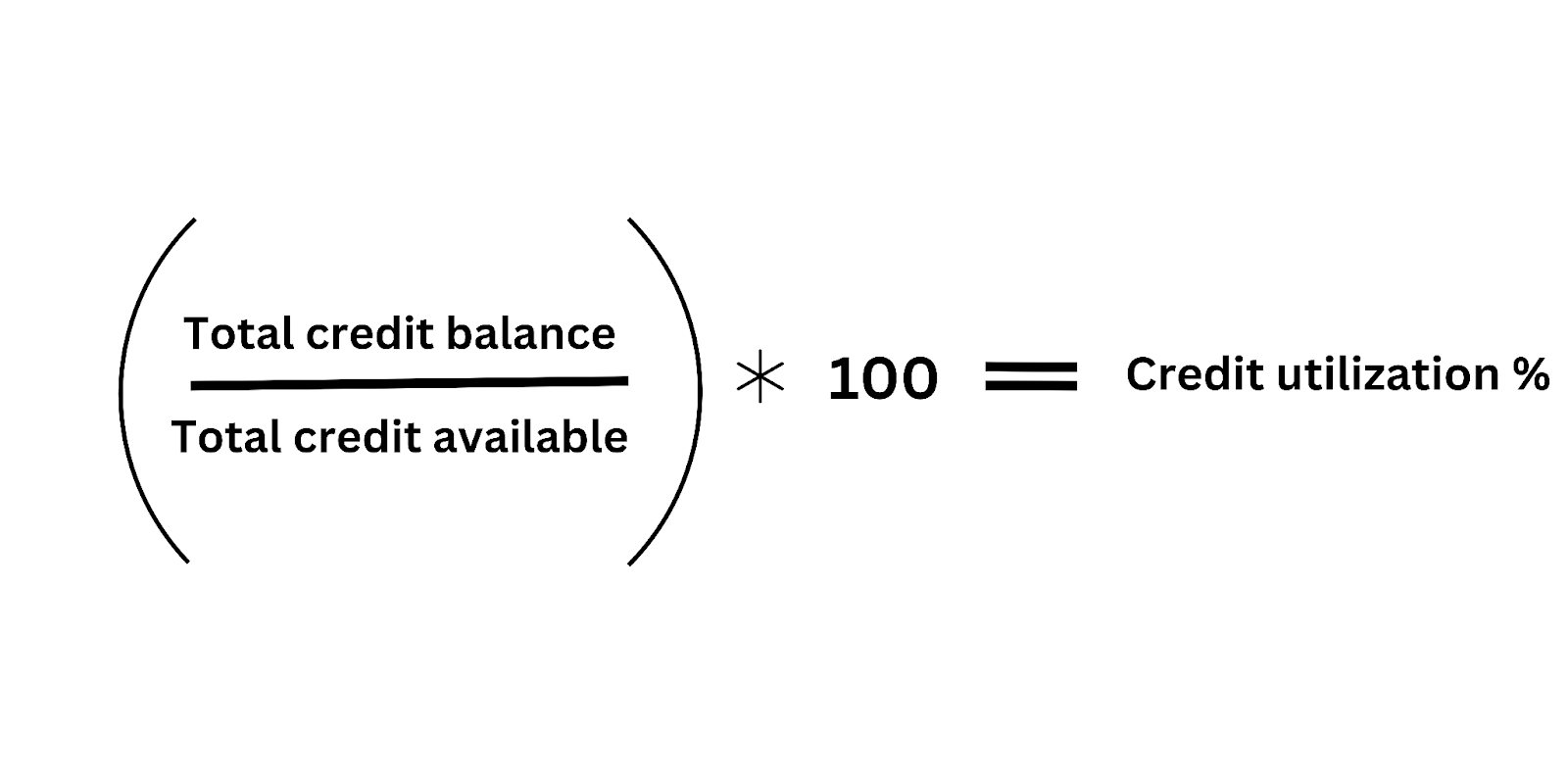

To calculate your credit utilization ratio, simply sum up your outstanding debts and divide them by your total available credit, then multiply the result by 100 to get the percentage of credit used.

For instance, if you have $1,000 in unpaid credit card balances and a combined credit card limit of $ 4,000, your credit utilization ratio would be:

($1,000 / $4,000) × 100 = 25%

How does your credit utilization ratio impact your credit score?

Your credit utilization ratio is of great interest to lenders as it reflects your ability to effectively manage your existing debt and serves as an indicator of your potential to repay any additional borrowed funds.

For instance, if you have multiple credit cards, some with balances nearing the credit limit, lenders may interpret this as a sign of financial strain and potential payment reliability issues, making them hesitant to extend further credit. On the contrary, a low credit utilization ratio assures lenders of your repayment capacity and indicates your ability to handle additional debt while meeting your financial obligations.

How to improve your credit utilization ratio

Increase your credit limit

Improving your credit utilization ratio can be as simple as requesting an increase in your credit limits. You can obtain extra credit either by opening a new credit card or by requesting an increase in the credit limit on one of your existing accounts.

If you're a long-standing customer who consistently pays off balances, your request is likely to be well-received. In some cases, your credit issuer might even proactively offer a limit increase.

Keep in mind that this process involves a credit evaluation, considering factors like income and credit history. It's essential to note that requesting a credit limit increase may require a hard inquiry, causing a temporary dip in your credit score as assessed by credit bureaus.

Pay your credit card balance

In order to gradually increase the available credit, make an effort to reduce your credit card debt as much as possible. Ensure you are aware of the billing cycle for each account and set up monthly due date reminders on your calendar. Ideally, aim to pay the full balance on your statement before the due date.

If you have multiple credit cards, it's wise to distribute your payments across all of them, as this improves the utilization ratio on each card rather than focusing on just one. Certain credit scoring models assess utilization across all your credit cards in order to calculate your credit score.

You can also inquire with your lender about the reporting schedule to the major consumer reporting agencies and then quickly settle your bill just before that reporting date.

Do not close unused credit cards

Avoid closing unused credit cards, even as you work on improving your credit profile. While it may seem tempting to close credit cards that you no longer use, doing so can reduce your total available credit and increase your credit utilization rate. It's typically advisable to keep older credit cards with no annual fees open.

The impact of closing an account can vary depending on the specific credit scoring model. For instance, certain credit-scoring models take into account the age of your oldest active account. Closing such an account could potentially lead to a decrease in your credit scores.

Reduce your expenses

If you're actively tackling credit card debt and find it challenging to make early or substantial payments, refraining from using your credit cards for purchases can be beneficial. Otherwise, any new charges could counteract your payments, hindering a reduction in your credit utilization rate.

Check and manage your credit utilization

Keep a close eye on your credit utilization by frequently reviewing your credit card balances and credit limits. This practice will help you stay informed about your utilization rate and allow you to make necessary adjustments. A lot of credit card issuers provide online tools and mobile apps designed to help you monitor your credit utilization.

Consider opening a new credit card

Opening a new credit card can boost your overall available credit, potentially reducing your utilization rate. Keep in mind that the exact credit limit may not be known until your application is approved, as it depends on various factors, including your income and credit history.

However, approach this strategically and avoid accumulating additional debt. It's important to open a new card only if you can manage it responsibly.

By following these steps, you can effectively manage your credit utilization rate and maintain a positive financial profile. This, in turn, will enhance your access to credit and help you achieve your financial goals.

Browse By Category

JOIN THOUSANDS OF OTHER HAPPY CANADIANS